The Commission's May 4, 2026 simplification reduces annual compliance costs by €6.1 billion. The catch is that the savings flow almost entirely to small operators, downstream traders, and importers from low-risk countries. If your business is the one EUDR was designed to discipline, the work between now and 30 December 2026 has not been simplified.

On May 4, 2026 the European Commission published Report COM(2026) 191 final along with a draft Delegated Act amending Annex I of the EU Deforestation Regulation. The headline number is enormous: annual EUDR compliance costs are projected to fall from €8.1 billion to €2.0 billion. That is a €6.1 billion reduction, or 75% of the original burden, across the universe of in-scope operators.

The number is correct, but it describes an average. Averages do not tell you what your own programme saves. Once you decompose the €6.1 billion by which operators are being relieved, the picture changes.

Where the €6.1 billion actually lands

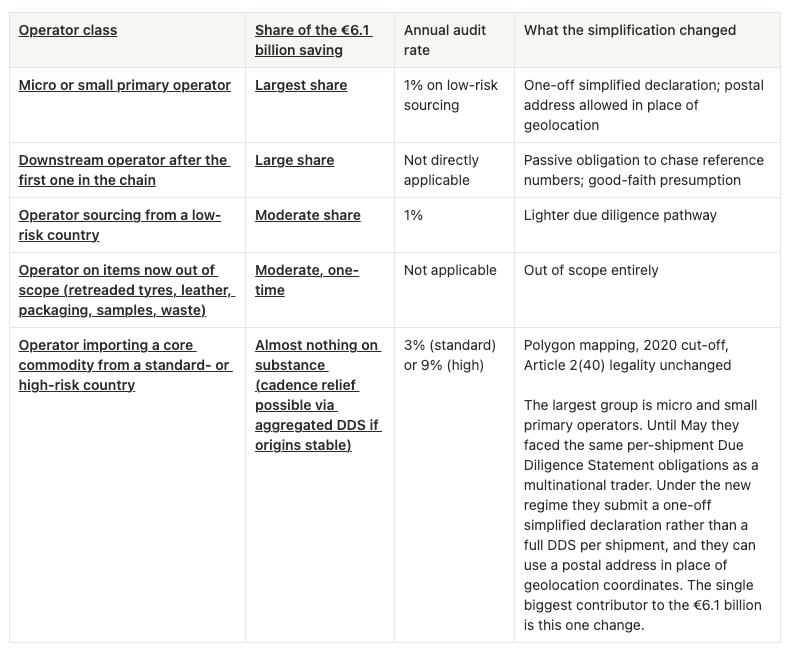

The Commission's report, together with the legal analyses that followed it ( Hogan Lovells , Baker McKenzie , Compliance & Risks , Ropes & Gray ), names four groups of operators that absorb most of the savings.

A practical qualification reinforces the asymmetry. To use the simplified pathway, the small operator must itself be the entity placing the product onto the EU market. Non-EU smallholder farmers almost never act as their own Importer of Record. They sell to middlemen, and the EU importer remains on the hook for the full DDS and GPS polygons. The simplification benefits EU-based farmers and foresters in practice, not the non-EU smallholders who supply the bulk of cocoa, coffee, palm, soy, and rubber into the EU.

The second group is downstream operators that sit beyond the first one in a supply chain. The Commission has clarified that their obligation to chase upstream DDS reference numbers is passive: if a downstream actor receives no reference number, it can assume in good faith that its supplier was not an upstream operator and move on. That clarification lifts a layer of paperwork off companies with no real production-level visibility in the first place.

The third group is anyone sourcing from a country the Commission has classified as low-risk. More than 140 countries fall into that category, including all EU Member States, the UK, the US, Japan, Australia, and South Africa ( country classification list ). Audits hit 1% of those operators per year, and the simplified due diligence pathway available to low-risk sourcing reduces documentary burden at the margin.

The fourth group is everyone whose products have been removed from Annex I. The draft Delegated Act, on which public feedback closes June 1, 2026, takes retreaded rubber tyres out of scope along with cattle hides, skins, and leather. It also carves out horizontal exemptions for samples, packaging, marketing materials, waste, and used or second-hand products.

There is a fifth group of operators whose evidence work the simplification does not reduce. It is the most important group for the regulation's enforcement target.

All groups benefit from one more simplification. The annual aggregated DDS, sometimes called the unchanged-origins rule, lets any operator with stable origins file one DDS per year per origin combination instead of one per shipment. It applies across all risk tiers, and reduces submission cadence without changing the evidence requirements underneath.

The companies the simplification does not reach

EUDR was written to discipline operators importing one of the seven core commodities (soy, palm oil, cocoa, coffee, rubber, cattle, or wood) from a country the Commission has classified as standard-risk or high-risk. Brazil sits in standard-risk. So do Indonesia, Malaysia, Côte d'Ivoire, Ethiopia, Argentina, Colombia, Mexico, and Peru. Only Belarus, Myanmar, North Korea, and Russia sit in high-risk. A company importing cocoa from Côte d'Ivoire, soy from Brazil, palm oil from Indonesia, or cattle from Brazil belongs in this fifth group, and almost none of the €6.1 billion belongs to them.

The fifth row of the table is the one that matters most for the regulation's target audience. Compliance leaders at these operators have spent the past three weeks asking their teams whether the 4 May headline applies to their own programme. For anyone whose EUDR exposure is on a core commodity from a non-low-risk source, the answer is no on substance. The geolocation requirement is still there, the polygon requirement is still there, the check for deforestation after 31 December 2020 is still there, the legality evidence is still there, and the DDS submission is still there (the cadence can drop if origins are stable; the underlying evidence does not).

What the simplification leaves untouched

For an operator in that fifth group, the May package leaves five things exactly as they were:

- Plot-level geolocation under Article 9. Latitude and longitude at six decimal places. Polygons for any plot larger than four hectares, for any commodity other than cattle ( Green Forum guidance ).

- The 31 December 2020 cut-off. Anything produced on land deforested or degraded after that date is non-compliant. The simplification does not move that line.

- The Article 2(40) legality check. Eight components: land use rights, environmental protection, third-party rights, labour rights, tax, anti-corruption, customs, and trade. Every in-scope shipment must carry evidence against all of them.

- The country-risk audit rates. They remain at 1% for low-risk, 3% for standard, and 9% for high-risk. The first scheduled review of country classifications is due in 2026, but the Commission has not published a date.

- The application date. 30 December 2026 for large and medium operators, 30 June 2027 for micro and small operators outside the timber sector. From the date of this post, seven months.

Why the simplification stops where it does

The four groups that benefit have one thing in common: the costs being relieved are administrative. Each of them was bearing paperwork to submit, reference numbers to chase, or scope ambiguity to interpret. The simplification reduces that administrative work, and the reductions add up to most of the €6.1 billion.

The costs the simplification does not touch are different in character. They are the costs of producing evidence about specific pieces of land. Where is the plot? What does its polygon look like? What was on it on 31 December 2020? Who holds legal title to it, and were the right environmental and labour rules followed in producing the commodity there? Those questions are not paperwork. They are about the observable physical reality of a specific patch of ground, and answering them requires satellite analysis, field verification, and supplier engagement. The Commission has not made any of that work cheaper.

EUDR demands evidence about the land the supply chain depends on. The May update does not touch that demand.

The numbers underneath the headline make the same point. The Commission has not refunded the CHF 2 million-plus that Barry Callebaut spent with partners on GPS-mapping cocoa farmers . It has not reduced the per-tonne compliance estimates that industry analyses now put at €15-40 in cooperative supply chains and €40-80 in intermediary supply chains across cocoa, coffee, and palm. The GlobalData study estimating $1.5 billion in EUDR consumer cost pass-through on cocoa and palm oil alone predates the May package and is not contradicted by it.

What to do before June 1, 2026

Six days remain until the Delegated Act feedback window closes on June 1, 2026. After that date, large and medium operators work under whichever version of the simplification the Commission finalises.

If you run compliance, sustainability, or trade at an in-scope operator, take your EUDR programme apart and label each line item by the categories above. For lines that are genuinely micro or small, downstream, low-risk-sourced, or now out of scope, real cost reduction arrives over the next eighteen months. The Commission's headline holds for those lines.

For the lines that involve a core commodity moving from a standard- or high-risk country into the EU, treat the simplification as having no effect. The plot-level geolocation, the polygon mapping, the 31 December 2020 status check, the legality evidence, and the DDS preparation are all still on the critical path to 30 December. The data layer or supplier system you rely on to produce that evidence has not been made optional by the package.

The €6.1 billion saving lands on a different group of operators than the ones EUDR was written to discipline.

Subscribe to our newsletter to get the latest on supply chain risk management, EUDR, deforestation, water stress, and the latest trends in geospatial AI.

Sources

- European Commission Report COM(2026) 191 final on EUDR simplification, 4 May 2026

- ESG Today, EU Commission Says Simplification of EUDR will Cut Costs by 75%

- Hogan Lovells, EU Deforestation Regulation: Commission Publishes Simplification Package

- Baker McKenzie, EU Commission Publishes Simplification Review of EUDR

- Ropes & Gray, EU Deforestation Regulation Update

- Compliance & Risks, EUDR Simplification Review 2026

- ICIS, EUDR simplification measures published

- Customs Support Group, EUDR Country Risk Tiers

- European Commission Green Forum, EUDR traceability and geolocation guidance

- European Commission Green Forum, EUDR country classification list

- Food Expo Connect, EUDR 2026 Compliance Guide for Food Exporters (per-tonne estimates)

- Confectionery Production, EUDR consumer-cost analysis (Barry Callebaut spend)

- GlobalData, EUDR consumer cost study